Need Truckload Carrier Capacity? Diversify

Is the longest run of supply/demand balance since deregulation ending? As balance/price tensions mount, shippers seek assured capacity and predictable costs.

The Bureau of Transportation Statistics continues to forecast that tonnage is increasing, but carriers seem to be replacing aging equipment rather than adding to their fleet sizes.

It appears that capacity is tightening, but it is unclear how sustainable recent trends are. Uncertainty is leading businesses to increase their access to capacity and minimize volatility in price.

What can you do to prepare for what’s next?

No one really knows what will happen to capacity in the coming months. It is unclear how quickly the economy will improve, thereby increasing pressure on available equipment, or whether/how much demand might outstrip supply and increase rates.

But shippers still have options—if they’re willing to reconsider their carrier procurement strategy.

Many shippers pursue a core carrier strategy, limiting themselves to working with a finite number of core carriers. Some take it a step further, working only with the very largest carriers—the ones with the most equipment.

The idea is to gain access to a huge pool of equipment and leverage their volumes for better rates. Other reasons for a focused carrier strategy can include operational efficiency within the drop trailer yards and shipping docks.

That strategy may work for 80% of their freight. The challenge with capacity and price volatility often comes with the remaining 20%. Here’s why.

- Approximately 93% of the truckload carriers in the U.S. are small carriers with 20 or fewer trucks; 75% have less than 5 trucks.

- Carriers are increasingly selective, with corridor and volume commitments that contribute to highest fleet efficiency. Meaning that volume for the sake of volume may not be attractive.

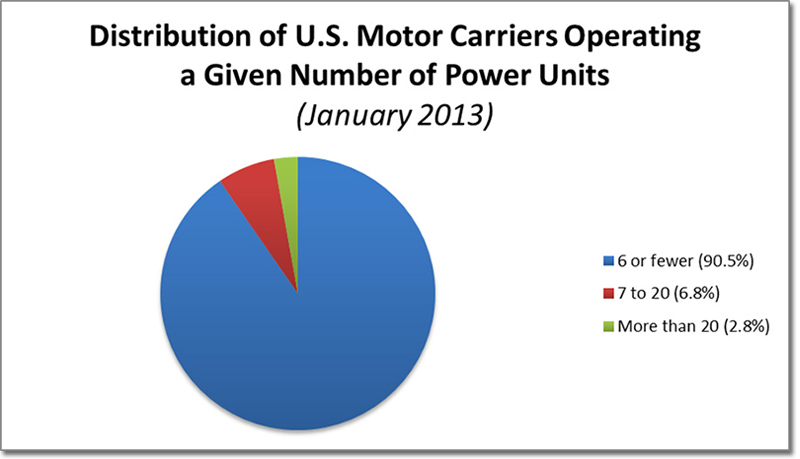

In their 2013 report, the American Trucking Associations (ATA) published the breakdown of carriers by pieces of equipment. Notice that the 2.8% of the carriers in the market that are listed as “large” have 20 trucks or more in their fleets; the subset of carriers with hundreds or thousands of pieces of equipment might represent an extremely small segment of the for hire carrier base. [1]

*Note: Chart includes private, for-hire, and motor carriers who did not specify their segment, but gave their fleet size. All other categories were excluded. Source: Federal Motor Carrier Safety Administration, U.S. Department of Transportation

- There are only 625 U.S. motor carriers with fleets bigger than 500 power units. [2] There are over 266,000 manufacturers alone, according to the National Association of Manufacturers, and that doesn’t even include other shippers like retailers and growers.There are only 625 U.S. motor carriers with fleets bigger than 500 power units. [2]

Large carriers often prefer regular freight in consistent lanes, so once they drop off a load, they can plan another will be available nearby for pickup. Increasingly, they are not interested in loads that don’t fit into their service network because these loads create inefficiency or lower yield.

Smaller carriers serve three vital functions:

- They travel to smaller, niche locations that bigger providers don’t service.

- They add elasticity to the market in dense corridors.

- They can be added to a shipper’s carrier base to help address lumpy demand and short lead time.

The opportunity to access capacity and minimize price volatility is to think small. Making use of smaller providers enables shippers of any size to introduce elasticity to their shipping and increase their access to available equipment.

While it may not be practical for you to manage relationships with several small carriers, you can call on a third party logistics provider (3PL) and integrate their service strategically into your transportation plan.

Third party logistics providers aggregate equipment, business processes, and price volatility for thousands of small carriers, yet give shippers a single relationship to manage. And 3PLs that work with the growing number of minority carriers offer a ready solution for shippers that have minority supplier initiatives. That generates positive returns for all parties involved.

As the balance between supply and demand seems to be changing in 2014, shippers who design a transportation strategy that balances their operations and supply chain needs with market capabilities will obtain the greatest flexibility and performance.

Have you sought out new capacity strategies for this year? Are you thinking small?

You can learn more about this topic by downloading the white paper, Strategies for Transportation Spend: Understanding the Dynamics of Carrier Pricing, Service, and Commitment.

1. American Trucking Associations. “2013 American Trucking Associations Report.”

2. U.S. Government Accountability Office. “Modifying the Compliance, Safety, Accountability Program Would Improve the Ability to Identify High Risk Carriers.” February 2014.