State of Logistics 2021: Air Cargo

Air cargo continues steady climb in volumes, rates.

Air Cargo continues to be the bright spot for aviation in terms of demand, but capacity remains tight, and shippers are paying higher rates.

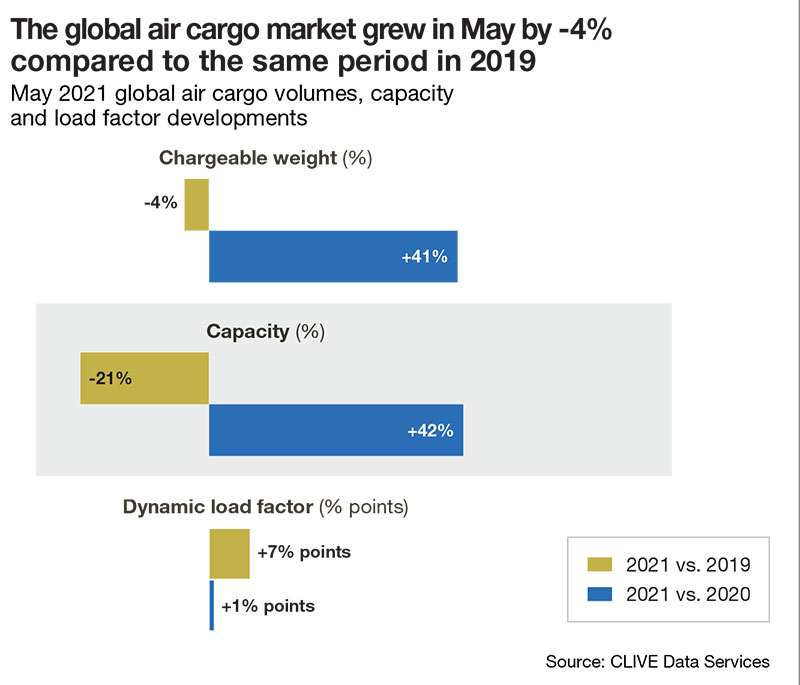

Data collected by the International Air Transport Association (IATA) and air cargo data services firm CLIVE over the past year show an upward trajectory in demand for air cargo services, although it did dip 4% in May. IATA attributes this to heightened global industrial production and cross border trade.

“Supply chain disruptions and the resulting delivery delays have led to long supplier delivery times—the second-longest in the history of the manufacturing PMI,” states IATA. “This typically means manufacturers use air transport, which is quicker, to recover time lost during the production process.”

Further data collected by CLIVE for April 2021 indicates air cargo volumes up 78% compared to April 2020 and up 1% compared to April 2019. CLIVE analysts emphasize how high load factors continue to strain international air cargo particularly given that the traditional surge in summer capacity has so far failed to materialize.

Analysts at CLIVE state that while April 2021 volumes may be close to those of April 2019, overall capacity was down 18%. For May 2021, available capacity was down 21% compared to May 2019. “This shows the gap in airline capacity is widening again compared to pre-pandemic market conditions following the -18% figure in April and -14% for March,” according to the analyst report.

May 2021 data versus the same month of 2020, when COVID restrictions caused severe disruption to the global aviation market, show +41% growth in chargeable weight, a +42% rise in available capacity, and +1% point increase in dynamic loadfactor. The “dynamic loadfactor” measures how full an aircraft is by considering both freight volume and weight.

“Airfreight capacity is still scarce on many key trade lanes, so prices remain strong as economic activity picks up while passenger air capacity remains constrained due to restrictions on international travel,” says Gareth Sinclair of air cargo market intelligence firm TAC Index. “The Baltic Air Freight Indices [weekly transactional rates for general cargo as provided by freight forwarders] increased by 3% in May over April, but this is a slowdown on the 17% growth seen in April over March.”

According to TAC, pricing strength continues on routes between China and Hong Kong to the United States and Europe, and from Europe to the United States. The airfreight market, particularly China and Hong Kong to the United States, also continues to be strong.

Sinclair surmises that this is likely to continue for some time as demand in several markets continues to outstrip supply. The result is that e-commerce traffic continues to increase and economic activity is strengthening in many markets.