Maxed out: 2014 Warehouse/DC equipment survey

Modern’s annual look into spending plans inside the four walls highlights growing interest in automation and software as workforce issues factor heavily into equipment investments.

Over the last few years, the results of Peerless Research Group’s (PRG) State of Warehouse/DC Equipment and Technology Survey have reflected an industry scrambling to adjust.

The recession, the e-commerce boom and advances in materials handling equipment and software have rewritten the rules on what seems like an annual basis. Just since 2010, the average anticipated spending on such equipment has spiked by 15% or fallen by 26% from one year to the next.

Whatever survey respondents are doing with their money, it seems to be working. Activity levels as a percentage of capacity are at their highest since at least 2007, while 95% of respondents believe that their activity levels will increase (by an average of more than 20%) or stay the same in the next two years.

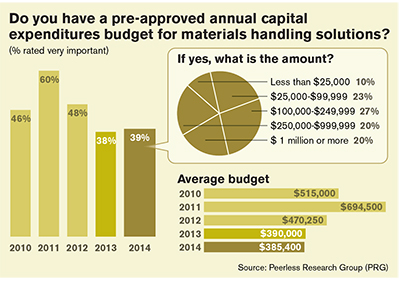

Yet, even as the number of potential investors taking a “wait-and-see” approach declines from 50% to 43% and the number “proceeding with investments” jumps from 19% to 27%, spending figures have been trending downward. Having spent heavily to get going, the industry is now transitioning to targeted investments aimed at keeping things on course.

Continued interest in automation

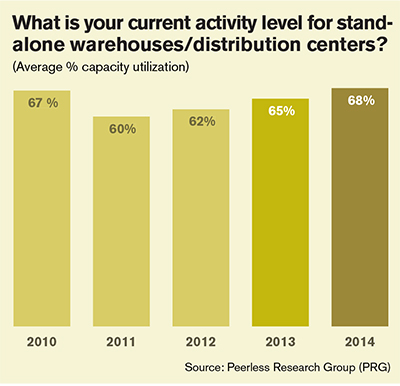

We know activity levels have grown in manufacturing (75%, up from 63% in 2012), warehousing supporting manufacturing (69%, up from 56% in 2011), and standalone warehousing (68%, up from 60% in 2011). That growth is largely due to a focus on doing more with less—optimizing existing facilities instead of new building. Technology and equipment investments have already helped support data-driven improvements, but many respondents feel there is much more to be done.

“Technology is expected to become even more critical in the upcoming years as a growing percentage of operations plan to automate inventory control and handling, distribution processes and labor management,” says Judd Aschenbrand, director of research for PRG. “In warehouses and DCs, continuous improvement, workload planning and lean processes are key initiatives going forward.”

The survey results point to significantly increased interest in automated processes in the next two years. There are sizable gaps between the number of respondents currently using automation to evaluate productivity in various functions and those who expect they will have transitioned to automated approaches within the next two years.

Those soon-to-be-automated functions include the tracking of inventory levels (58% currently automated, 76% in two years), order fulfillment costs (40%, 60% in two years), and daily throughput (44%, 69% in two years).

This shift is reflected in the increased percentage (54%, up from 50%) of respondents who plan to invest in information technology hardware or software in the next 12 months. But respondents are also keen to optimize the productivity of each and every worker, anticipating growth in automated tracking of picking accuracy (33% currently automated, 62% in two years), labor hours (51%, 69 percent in two years) and on-the-job injuries (18%, 37% in two years).

Investing to curb workforce challenges

The growth of multi-channel distribution and e-commerce have pressured the distribution center and supply chain to run more efficiently, according to Norm Saenz, managing director at supply chain consultancy St. Onge.

“In an effort to cut operating costs, some might have performed layoffs in recent years,” Saenz says. “Now that activity levels are up, the back is breaking in many facilities, and thus the willingness to spend on automation to enhance the productivity of those workers. But while technology and automation receive the headlines for improvement in operations, more businesses understand it’s the labor force that sustains productivity and high service levels.”

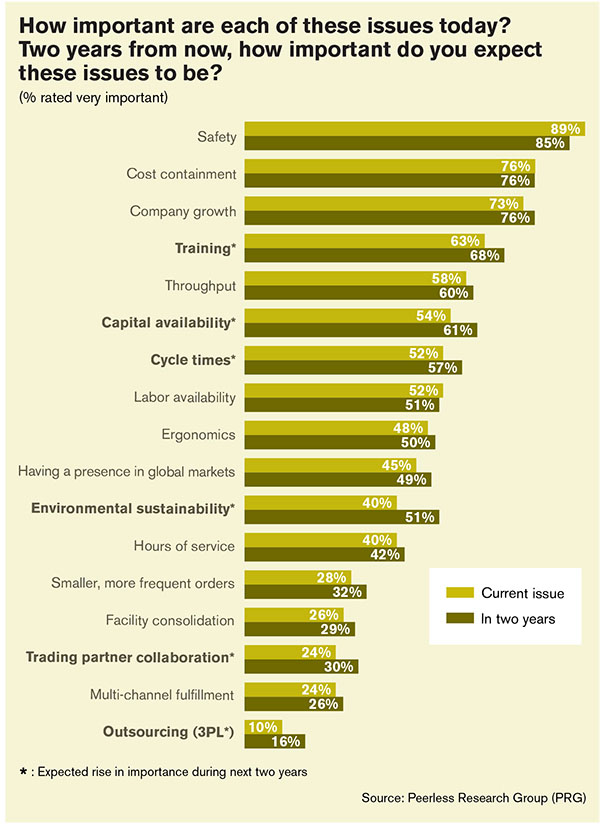

When asked to identify the issues that are most relevant now and to estimate their relevance in two years, 89% of respondents again placed safety at the top of the list. Just two years ago, cost containment topped the list, but it now sits in second place with 76%. Labor-related issues like training (63%), labor availability (52%) and ergonomics (48%) are expected to become more pressing in coming years.

“The sophistication of the skill sets required to operate leading-edge equipment and system solutions in the material handling, logistics and supply chain industry will require an equally sophisticated and well-trained workforce,” says George Prest, CEO of supply chain association MHI. “Hiring, training and retention of workers is the most important issue facing this industry.”

But none of the listed issues saw a greater jump in anticipated relevance than environmental sustainability. Currently, 40% of respondents see it as an important issue, and 51% believe it will be within two years.

“Because they are elective and not mission-critical, green initiatives go hand in hand with how well the global economy and the individual company are doing,” says Aschenbrand.

Supply chain visibility

In a new question added to the survey this year, respondents were asked about the level of end-to-end visibility across their supply chains.

An impressive 36% indicated that they have full end-to-end visibility across their supply chains, while another 27% described their manufacturing and warehousing operations as a group of discrete silos. In the middle, 61% stated they are in the process of improving integration among supply chain nodes. “End-to-end supply chain visibility will be a requirement for future supply chains,” says Prest.

For example, the multi-channel model requires it, says Prest. “While many companies have traditionally maintained dedicated facilities to serve demand from specific channels, companies adopting multi-channel strategies must maintain real-time visibility of inventory at different facilities and synchronize operations across the supply chain,” he says. “This visibility will improve efficiencies by maintaining one common pool of inventory.”

Cloud-based or software as a service (SaaS) approaches are gaining some ground in this space, although overall adoption remains modest. Only about a third have either adopted (13%) or are currently evaluating (18%) SaaS or cloud computing strategies. And, 20% have determined “it’s not for us,” 36% aren’t sure of their company’s interest, and 10% are not sure what cloud computing is.

“Those who are adopting these strategies cite cost savings, data reliability across the enterprise, streamlining of operations, ease of information access, and improved communications with customers and suppliers,” says Aschenbrand. “But concerns over security, privacy, data integrity and system reliability remain as reasons for non-adoption.”

Software: Cornerstone for improvement

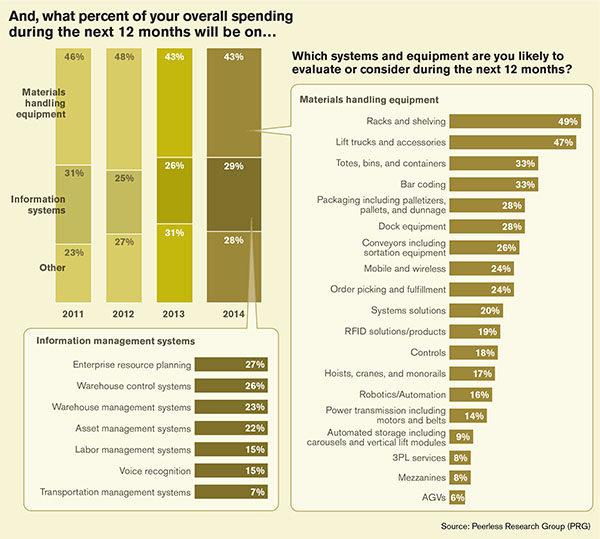

In the next 12 months, 43% of planned spending will go toward materials handling equipment like racks and shelving (49%), lift trucks and accessories (47%), bar coding (33%), conveyors and sortation (26%), mobile and wireless solutions (24%), and robotics and automation (16%).

In past years, investment in equipment might have been independent from investment in information technology solutions, but Saenz says that’s no longer the case.

“There is a close relationship between equipment and IT investments,” says Saenz. “At some point, when automation is included in the investment, certain software and handling control systems are required to efficiently manage the automation. Generally, as the investment in equipment and IT increases, the relationship becomes much closer between the two.”

Planned spending on information technology suggests businesses will work to improve the collection and management of data from every corner of the supply chain. In the next year, roughly a quarter of respondents will invest in each of the following: enterprise resource planning (ERP), warehouse management systems (WMS), warehouse control systems (WCS), and asset management systems. Labor management systems (15%), and voice recognition technologies (15%) also placed high on the list.

“WMS has evolved into a sophisticated $1 billion-plus industry that operates in a highly competitive environment,” says Prest. “The top providers have expanded their solution offering beyond the warehouse and the term ‘supply chain execution’ has been widely adopted to reflect the shift to more comprehensive logistics applications. Thus, the WMS category for this type of solution may be too limiting.”

For companies not yet ready to shed their legacy WMS, Saenz says that many can enjoy strong returns from bolt-on modules. “At a fraction of the investment, an LMS can greatly improve the control and productivity of the labor force, and stronger inventory management module can be a significant cost savings opportunity,” he says. “This could be a Band-Aid approach to enhancing their systems, should the company replace the entire WMS in the future.”

As they move forward with information technology initiatives, 61% of companies prefer to work with a suite of applications from a single vendor, as opposed to the 39% who prefer a best-of-breed strategy employing software from various suppliers.

Once businesses have established a solid baseline of internal data, they will expect trading partners to be able to share comparable information. Today, 24% see trading partner collaboration as an important issue and 30% expect it to be more important in the next two years.

Respondent demographics

In December, Peerless Research Group (PRG) e-mailed survey questionnaires to readers of Modern Materials Handling, yielding 412 qualified respondents from manufacturing (36%), warehousing (22%), corporate (26%), and aligned logistics professionals (15%).

The median revenue of responding companies is $91.9 million. Qualified respondents—those managers and personnel involved in the purchase decision process of materials handling solutions—hold influence over an average of 136,885 square feet of warehouse or DC space.