2018 Rate Outlook: Economic Expansion, Pushing Rates Skyward

Trade and transport analysts see rates rising across all modes in accordance with continued expansion of domestic and international markets. Economists, meanwhile, say shippers can expect revenue growth in transport verticals to remain in the 3%-plus range.

The best global growth rate in seven years—3.2% in 2017—is based on firm foundations, contend leading economists. They add that, barring a significant shock, this current expansion has plenty of “staying power” and should continue to push rates up and keep capacity constrained around the globe.

According to Nariman Behravesh, chief economist at IHS Markit, macroeconomic policies remain growth-supportive, notwithstanding a gradual “normalization” of monetary policy. “Europe continues to surprise on the upside,” says Behravesh. “Japanese growth is solid, albeit slower than most. China’s growth is holding up thanks to stimulus, and the emerging world is coming out of a two-year growth slump. Excluding a distraction, this expansion can continue for at least a couple more years.”

Register for the Rate Outlook Webcast here.

While there is no shortage of low-probability/high-impact risks (e.g., North Korea), the biggest threats to world growth are “policy shocks,” says Behravesh, who maintains that, in the past, central banks have tightened policies too much either prematurely or too late. “And with inflation somewhat calm as this time,” he adds, “the risk of tighter monetary policy killing off this expansion remains low.”

Sara Johnson, executive director of global economics at IHS Markit, observes that, in the U.S. third-quarter, real GDP growth was reported at a solid 3% despite disruption stemming from hurricanes Harvey and Irma.

“Were it not for the hurricanes, GDP growth in the third quarter could have registered 3.5%,” Johnson adds. “At this time, the underlying momentum in the economy is strong, and we forecast real GDP growth of 2.2% in 2017 and 2.5% in 2018—and this lowers the unemployment rate to below 4% in late 2018.”

Energy getting expensive

No discussion of macroeconomic pressures can unfold without considering energy. As they did last year across the board, analysts expect rising fuel costs to have an impact on how shippers select modes in the next 12 months.

Derik Andreoli, Ph.D.c, director of economic research and forecasting at Mercator International and the “Oil and Fuel” columnist at LM, observes that oil prices have been rising steadily since late June and will set the tone for 2018.

“The fundamentals support a bullish outlook,” says Andreoli. “Global demand looks to grow between 1.4 million barrels and 1.6 million barrels per day, while the oil surplus that hung over producers at this time last year has disappeared—despite the fact that U.S. shale oil production grew by more than 900,000 barrels per day over the course of the year.”

Consequently, the direction of the oil market is largely in the hands of Saudi Arabia, and to a lesser extent, Kuwait, as these are the only OPEC producers that have adhered to the agreed cuts in any meaningful manner. “Had these two continued in 2016 to produce oil at the average rate they each achieved in 2015, the market would still be oversupplied by around 560,000 barrels per day,” says Andreoli. “While a handful of other OPEC members now produce fewer barrels than they did in 2015, these countries are suffering long-term production declines.”

According to Andreoli, predicting a price this year is complicated by the return of the “swing producer,” or suppliers that possess large spare production capacity. At what price, for example, will Saudi Arabia let the taps flow more freely? “Given the current trajectories of global supply and demand,” he says, “it’s easy to see oil prices rising above $70 by mid-year, and this upward momentum could continue if the global economy continues to chug along its current path.”

“At this time, the underlying momentum in the

economy is strong, and we forecast real GDP growth

of 2.2% in 2017 and 2.5% in 2018—and this lowers

the unemployment rate to below 4% in late 2018.”

Also, Saudi production increased in both the second and third quarters of 2017, and this trend appears to be holding through the fourth. “It appears that the Kingdom is happy to lift production so long as oil prices increase,” says Andreoli. “This does not bode well for consumers, as prices might surpass the $70 barrel mark to end 2018 on an even higher note.”

Upward pressure on prices might be mitigated if substantial oil volumes suddenly appear from “drilled but uncompleted” wells, he says—but he’s not making that bet yet.

Trucker’s market in 2018

After much anticipation, “a trucker’s market” is due to arrive in 2018, says Stifel Nicolaus trucking analyst John Larkin—although he cautions that supply/demand is already tight across the industry as the domestic economy continues to grow at a slow, yet very steady pace.

“The primary driver of the supply/demand tightness is the economy-wide shortage of skilled, blue collar labor,” says Larkin. “It has become very challenging to find drug-free, compliant drivers given today’s driver wages. And while driver pay scales began to rise in the second half of 2017, the starting point for wages was so low that it may take multiple wage hikes before we see any alleviation of this chronic challenge.”

Larkin notes that on December 18, 2017, the electronic logging devices (ELD) mandate was fully implemented. This, he cautions, may “add insult to injury,” further compressing an already tight market.

Meanwhile, truckload (TL) rates are soaring. Larkin recalls that he first witnessed “an inflection” in spot rates in mid-2016. He adds that normally contract rate increases follow with a six-month lag. Recently however, this cycle extended for over a year.

“The hurricanes in the third quarter were the catalyst that tightened an already tightening market,” says Larkin, “giving carriers the confidence to push for and receive upper single digit rate increases. And, with the advent of the ELD mandate, additional rate increases may be forthcoming.”

This may be especially true for those shippers that treated carriers harshly over the past two years, Larkin adds. “Some shippers abandoned their collaborative approach and then resorted to old-fashioned rate reduction demands,” he says.

As a consequence, the positive rate environment will cut across all the TL sectors—dry van, reefer, flats, bulk—and could have staying power unless autonomous trucks are pressed into widespread service. This scenario, says Larkin is “unlikely.” Also, the chance that a much discussed apprentice program—allowing 18 year-old-driver apprentices into the industry—comes into play is another long shot next year.

Larkin observes that the less-than-truckload (LTL) industry, which is much more consolidated than the highly fragmented TL sector, has seen rates rise modestly over the past couple of years, even as TL carriers succumbed to widespread pricing pressure.

“However, reports have surfaced recently suggesting that LTL capacity is becoming scarce in some regions of the country,” adds Larkin. “It seems that LTL carriers are picking up some overflow freight from the truckload industry.”

In addition, LTL carriers are benefitting from the growth of e-commerce and the automation of manufacturing. Larkin says that with no new entrants, he expects some acceleration in LTL rate increases.

Rail/intermodal reacts

A prominent industry analyst has observed that that 2018 is expected to be a much better year for railroads and the shippers that rely on them. Frank Harder, a principal with the transport consultancy Tioga Group, says that the inflection point was in late 2016, with railroads enjoying modest year-over-year increases throughout 2017.

Total U.S. carload traffic for the first 47 weeks of 2017 was up 3% from the same point last year; and intermodal units were up 3.7% from last year. “The industry has been experiencing record intermodal volume since mid-2017,” adds Harder.

As a result of a decade-long decline in coal and other rail traffic, railroads are still operating at approximately 80% of peak 2006 volume levels. Consequently, railroads generally have line and locomotive capacity to grow their traffic.

“Railroads are generally optimistic about increasing shareholder value in 2018 given the growing industrial economy, the prospect of tax reductions and the tightening of truck capacity,” says Harder. “Because there’s available operational capacity and because positive train control is coming on line, capital expenditures are expected to be relatively lower than in previous years. Surplus cash is going into dividends and share repurchasing.”

According to Harder, CSX is the “wild card” in the rail equation in 2018. “The carrier’s operational changes made in 2017 caused some service disruption, but that appears to be in the past and third quarter 2017 performance was better than the previous year.”

Harder says that shippers should expect a rationalization and simplification of CSX’s intermodal network in 2018 and perhaps a movement of emphasis away from hub-and-spoke operations toward dense point-to-point services. A key indicator of future direction, he says, will be CSX’s use of its Northwest Ohio Intermodal Hub.

“Motor carrier prices provide a ceiling for intermodal and truck competitive merchandise segments of the rail business,” Harder concludes. “My expectation is that rail and intermodal prices will increase with motor carriers to be about 1% to 2% above inflation.”

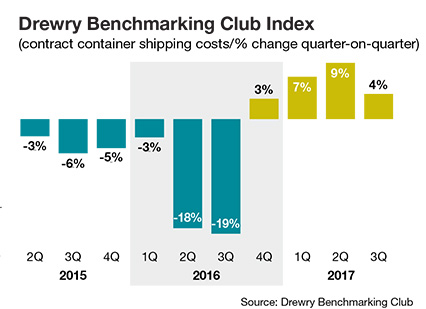

Ocean carrier “correction”

After the strong upwards correction of freight rates witnessed in global ocean container transportation during 2017, the question now is whether the trend will continue for another year or if rates will stabilize.

According to Philip Damas, director of London-based Drewry Supply Chain Advisors, one temporary factor behind the increases was the bankruptcy of Hanjin Shipping—then the 6th largest global ocean carrier—in September 2016.

According to Philip Damas, director of London-based Drewry Supply Chain Advisors, one temporary factor behind the increases was the bankruptcy of Hanjin Shipping—then the 6th largest global ocean carrier—in September 2016.

“There was a strong resulting surge in spot rates due to reduced capacity,” says Damas. “This resulted in a ‘fear factor’ among shippers who accepted higher prices to ensure continuity of service, and a change of behavior among ocean carriers who decided to move away from chasing market share at discounted rates and, instead, focus on carrying cargo at compensatory rates.”

Other factors indicating that the increases of 2017 will continue in 2018 include a return of higher trade volume growth and a further increase in fuel prices, among others. Drewry contends that some of these price drivers will continue to influence the direction of prices in 2018, whereas others were short term and will have no further effects.

“Despite the increase in deliveries of large containerships scheduled for 2018, we don’t expect a new price war in ocean transportation, as robust demand growth and higher carrier concentration will influence the market,” says Damas.

On average, freight rates in the global ocean transportation sector increased by about 10% when compared to the first three quarters of 2017 versus the same period a year earlier. “This was a reversal of the prior deflationary trend of ocean rates,” says Damas adds. “On the high-volume lanes from Asia to the United States and from Asia to Europe, increases in fixed annual contract rates of more than 30% were common, whereas rate increases on secondary lanes were marginal.”

However, a new trend since the fourth quarter of 2017 is that spot freight rates on these high-volume lanes from Asia to the Unites States and from Asia to Europe—which had been high for the 10 months after the Hanjin bankruptcy—have weakened quite a bit since July 2017. This leads some to expect that 2018-2019 fixed annual contract rates, when they’re negotiated in the next few months, will also be lower.

“Based on Drewry’s experience of managing ocean freight tenders and also using our forecasts and insights into the supply-demand balance and carrier costs, we warn manufacturers and retailers that further increases in spot rates of up to 10% are likely in 2018 if you do not ship under contract, but medium and large companies shipping under contract on the major lanes should be able to secure new contracts with average increases of about 5%, depending on the lane,” says Damas.

Drewry analysts maintain that “it’s unlikely” that further increases of more than 30% in contract rates will happen in the next year. There will be exceptions, like the Asia-U.S. East Coast lanes, where analysts expect that new market entrants will disrupt the market and trigger some rate decreases, and like the Europe-Asia and some North-South lanes, where there may be higher rate increases than 5%.

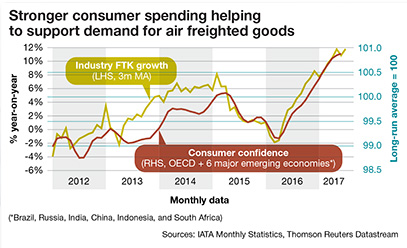

Recovery continues in air cargo

While the nation’s air cargo industry remains strong, several indicators suggest that demand may have passed the growth peak. According to The International Air Transport Association (IATA), the inventory-to-sales ratio in the U.S. is “tracking sideways,” signaling that the period when companies look to restock inventories quickly—which often gives air cargo a boost—has ended.

Meanwhile, the new export orders component of the global “Purchasing Managers’ Index (PMI)” is stable, while the upward trend in seasonally-adjusted freight volumes has moderated. With that, airfreight volumes are still expected to grow in 2018, though at a slower pace than 2017.

“Demand for airfreight grew by 5.9% last December says Alexandre de Juniac, IATA’s director general and CEO. “And tightening supply conditions in the fourth quarter should see the air cargo industry deliver its strongest operational and financial performance since the post-global financial crisis rebound in 2010.”

Indeed, for the past 15 months, demand growth has outstripped capacity growth—which is positive for load factors, yields and financial performance. Chuck Clowdis, managing director of consulting firm Trans-Logistics Group, Inc., observes that given the strong rebound in consumer confidence translating into robust consumer spending, air cargo “is enjoying a very fine holiday season again” this year.

“As unemployment numbers have fallen, we’ve seen a return to higher value goods,” says Clowdis. “This is despite some refinement of the definition of ‘high-value luxury’ items as defined in the past. As a consequence, the need to increase speed-to-market has played well for air cargo operators.”

Clowdis also notes that the mix of consumer goods and high-tech products has been strong and complement the usual mix of pharmaceuticals and critical parts air shipments. “Air cargo shippers should expect higher rates in 2018,” he adds, “so they had better develop sharper negotiating skills, commit to greater volumes and collaborate more closely with service providers.”

Parcel packs a punch

Of all of the transportation and logistics sectors relied on by shippers today, none will be more volatile than the parcel express market in 2018.

Analysts note that over the past 12 months, logistics managers have seen major changes in pricing from the parcel duopoly of FedEx and UPS; the accelerated emergence of regional parcel players; and the increasing power and reach of e-commerce giant Amazon as it grows its own delivery capabilities globally.

Meanwhile, Pitney Bowes recently announced a 48% increase in global parcel volume over the last two years, as reported by its second annual “Parcel Shipping Index.”

Parcel volume has grown from 44 billion parcels in 2014 to 65 billion in 2016, and the increase in growth shows no signs of slowing down, with the index estimating that parcel growth will continue to rise at a rate of 17% to 28% each year between 2017 and 2021.

Jerry Hempstead, president of parcel express analyst firm Hempstead Consulting, advises shippers to remain vigilant when it comes to negotiating rates this year. “Every shipper’s profile will vary, but in general the published ‘average’ increase should suffice for most,” he says. “We are again at the point where the FedEx base rates and the UPS base rates for the most part will mirror each other.”

As a result, the players have all announced similar average increases for 2018. There are some nuances, but Hempstead advises shippers to budget for at least a 4.9% increase in costs for 2018. “But as we have seen in the past, the devil is in the details, and the details will affect shippers to a lesser or greater degree depending on their mix of weights, zones, services selected and cube,” he says.

Under the greatest pressure in 2018 will be the value of size as carriers increase the penalties for over-packing and tendering larger packages, in particular non-conveyables.

“The big increase in cost will come in the form of both rule changes and fee increases for shipments that are defined as ‘additional handling’ and shipments deemed to be ‘oversized,’” says Hempstead. “Carriers can provide logistics managers with detailed reports of shipments that were tendered and charged for these fees in 2017. This will be essential for estimating future expenses.”