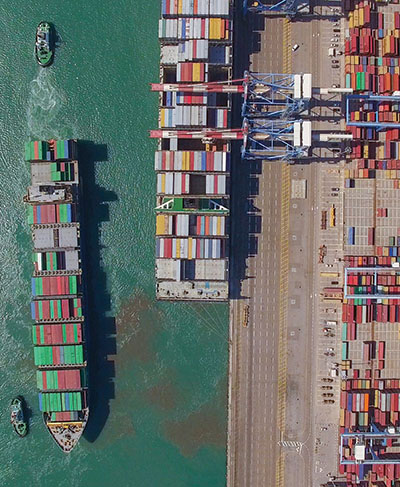

Ocean Carrier Trends: Containing capacity while remaining poised for growth

While the prospects for container shipping are brightening, downside risks of increased inward-looking policies and the rise of trade protectionism are weighing on the outlook for carriers.

Coinciding with the upswing in the world economy two years ago, global seaborne trade is doing well, note analysts for the Geneva-based United Nations Conference on Trade and Development (UNCTAD). They also observe that containerized shipping expanded by 4% in 2018—the fastest growth in five years.

“Global maritime commerce gathered momentum two years ago and raised sentiment in the shipping industry,” says Frida Youssef, UNCTAD’s trade analyst. “However, escalating frictions may derail the recovery.”

An immediate concern is the trade tensions between China and the United States, the world’s two largest economies, as well as those between Canada, Mexico, the United States and the European Union. There’s little doubt that trade wars in these arenas could reshape global maritime trade patterns and dampen UNCTAD’s cautiously optimistic forecast. According to Youssef, other factors driving uncertainty include the ongoing global energy transition, structural shifts in economies (China for example) as well as shifts in global supply chain development.

“If leveraged effectively, game-changing trends such as digitalization, e-commerce and the Belt and Road Initiative to increase infrastructure between China and the EU—the exact impact of which is yet to be fully understood—have the potential to add wind to the sails of global seaborne trade,” concludes Youssef.

Rate uplift

Shipping industry experts at the London-based consultancy Drewry concur with this analysis, but also note that, for the time being, healthy demand growth for containerized services is outpacing fleet expansion. That’s the good news contained in the latest edition of Drewry’s “Container Forecaster,” a report that adds that this may mean a better supply-demand balance and slightly higher freight rates and profits for carriers.

“The bad news for carriers is that they’re unlikely to see the very strong demand growth rates of early 2017 for the foreseeable future,” says Simon Heaney, senior manager of container research at Drewry. “Still, while port handling growth may have peaked, carriers can still expect more than adequate volumes for at least the next two years.”

Drewry maintains that subtle changes to the new vessel orderbook, mainly in the form of delivery deferrals, have softened this year’s new capacity burden and had a positive effect on Drewry’s supply-demand equations for 2019.

“Last year’s top-heavy delivery schedule with the majority of ultra large container vessels (ULCVs) being delivered in the first quarter of 2018 has depressed our supply-demand index,” says Heaney. “However, the balance will improve as the year progresses. Unfortunately for carriers, this won’t come soon enough to erase the negative sentiment for annual contracts.”

He adds that Drewry anticipates only a “small uplift” in average freight rates for the year.

Balancing act

Peter Sand, the chief shipping analyst for the Baltic and International Maritime Council (BIMCO) in Copenhagen reckons that global container fleets will grow 3% in 2019, which is just half the rate of 2018. He calls this a return to “fundamental balance,” which is likely to improve. BIMCO is the largest of the international shipping associations representing ship owners controlling 65% of the world’s tonnage. It has members in more than 120 countries, including managers, brokers and agents.

“Although container volumes fell off during the last six months of 2018, global fleets moved 125.2 million twenty-foot equivalent units (TEU) in the first nine months of the year,” says Sand. “This was an improvement of 4% over the first nine months of 2017.” He adds that orders have been placed for 1,176,000 TEU of new capacity this year, with most capacity driven by Hyundai Merchant Marine’s purchase of eight 15,300-TEU ships and 12 23,000-TEU vessels built in South Korea.

Most of the new orders are for delivery in 2020, when BIMCO expects more than one million TEU of new capacity to be delivered. So-called “mega-vessels” comprise 82% of those on order with a capacity of 11,000 TEU or more. Only 18% are for ships carrying 3,100 TEUs or fewer containers. “But next year, if the demolition level reaches higher than 100,000 TEU, fleet growth should stay below 3%—half that of 2019,” says Sand.

Pricing platforms

With pricing transparency becoming even more of an issue, third-party technology providers like INTTRA, CargoSmart and GT Nexus insist that carriers will become more networked in 2019. Shipper skepticism remains evident, however.

“We think it’s incredibly important for carriers to invest in more information technology that will help drive more transparency into the supply chain,” says Jonathan Gold, vice president, supply chain and customs policy for the National Retail Federation. “However, as we’ve seen recently, some carriers are pushing their own systems with no interoperability between them.”

Brendan McCahill, senior vice president at Descartes Datamyne, an import/export trade database provider, shares this view, noting that the majority of carriers understand the benefit of common platforms. “Just as the advent and expansion of vessel-sharing agreements have helped carriers control costs and improve services, more networked services will help carriers as well,” he says.

While IBM and Maersk are continuing to attract shippers as partners in its own blockchain, nine leading ocean carriers and terminal operators have signed a memorandum of understanding (MOU) to form a consortium to develop the Global Shipping Business Network (GSBN) that consists of an open digital platform based on distributed ledger technology—the foundation of blockchain.

“We are pleased to provide an industry-wide forum for collaboration,” says Steve Siu, chief executive officer of CargoSmart. “We feel that blockchain technologies can transform the shipping and logistics industry, thereby elevating supply chain processes.”

The other participants include ocean carriers CMA CGM, COSCO, Evergreen Marine, OOCL, and Yang Ming. These players have teamed with the terminal operators DP World, Hutchison Ports, PSA International Pte Ltd, and Shanghai International Port in the formation of the GSBN.

Based on blockchain technology, the new platform promises to offer the following benefits:

- a cooperative network that should enable members to develop applications and connect to other consortium networks to increase the speed of data integration and improve business performance;

- peer-to-peer networking to allow data owners to share immutable records to other shipment stakeholders, enabling them to take quick action regarding critical milestones and to keep cargo moving throughout the supply chain; and

- an industry-wide, common, trusted and expansive digital model designed to provide a foundation for initiatives and market intelligence.

Zim Lines, meanwhile, has opted out of the network, preferring to work with high-tech, third parties Wave Ltd. and Sparx Logistic to chart its own blockchain course by introducing paperless documentation.

However, does all of this collaborative innovation signal an end of carrier consolidation? A number of prominent freight intermediaries don’t think it will. “Although we can’t foresee any major deals in 2019, a full merger between carriers will take place in the near future,” says Serkan Kavas vice president, imports at MTS Logistics, a New York-based freight forwarder. “Independent carriers will be a particularly big target for larger players.”

At the same time, logistics managers should see more vessel-sharing agreements, with carriers seeking to differentiate their brands with “premium” service offerings. “Shippers are now expecting guaranteed loadings, faster unloadings and guaranteed transit times,” concludes Kavas, “While the leading carriers are working to become end-to-end logistics providers.”

Fuel for thought in 2019

As we usher in 2019, many industry analysts are telling logistics managers to begin planning for a major transformational event coming into play for the ocean cargo sector a year from now.

According to a recent survey conducted by global shipping consultancy Drewry, there’s “considerable unease” about the International Maritime Organization’s global emissions regulations, due to come into force on January 1, 2020.

Respondents in both the survey and follow-up interviews expressed particular concern about carriers’ methods of fuel cost recovery, with more than half (56%) stating that they did not consider their service providers’ existing approaches as either fair or transparent.

Respondents in both the survey and follow-up interviews expressed particular concern about carriers’ methods of fuel cost recovery, with more than half (56%) stating that they did not consider their service providers’ existing approaches as either fair or transparent.

Furthermore, four of every five shippers participating in the survey stated that they had yet to receive clarity from their providers as to how the widely anticipated future fuel cost increases, set to accompany the 2020 regulatory change, would be met.

Most alarming, perhaps, is the finding that a surprisingly large proportion—33%—admitted to having poor or very poor awareness and understanding of the new regulation.

In Drewry’s view, the level of uncertainty today concerning the total cost impact is so large that nobody is able to provide a confident forecast of the cost of compliance. According to the report, the only certainty is that the extra cost will run into billions of dollars globally come 2020.

Based on independent “futures” prices, low-sulphur marine fuel prices per ton will be 55% higher than current high-sulphur fuels, and Drewry considers that the probable worst case scenario is that fuel costs—paid by carriers—and fuel surcharges—paid by shippers—in global container shipping will increase by 55% to 60% in January 2020.

Philip Damas, head of Drewry Supply Chain Advisors, observes that the IMO low-sulphur rule represents a very significant, industry-wide “change event” that will likely have far reaching effects on the global shipping industry for many years to come.

“Given the scale of the extra costs triggered by the new regulation and the carriers’ expectations that their pricing and fuel charge mechanism with customers must be restructured, there is a need for carriers to address the transparency concerns expressed by their customers,” Damas adds.