Lift Truck Acquisition & Usage Study: Fleet managers in the driver’s seat

As they get their arms around technology, fleet management solutions and disciplined practices, fleet managers plan to continue reaping the rewards of targeted investment.

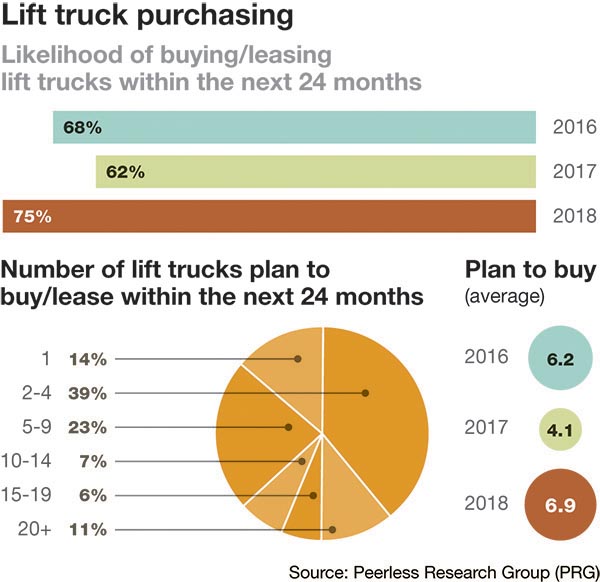

Following consecutive record-setting years, the lift truck industry looks set to record another banner performance. According to the results of Modern’s annual “Lift Truck Acquisition & Usage Study,” conducted by Peerless Research Group, three quarters of respondents expect to buy or lease a lift truck in the next 24 months.

Those surveyed plan to acquire an average of seven forklifts in the next two years, including 39% in the market for two to four units, 23% for five to nine, and 11% shopping for more than 20. After a brief dip in 2017, the average spend is back up to 2016 levels at $149,040, with 64% planning to spend up to $100,000 in the next 12 months, and 10% planning to spend between $250,000 to $1 million.

In addition to capturing plans to grow, replace and invest in forklifts, the survey sheds new light on fleet managers’ efforts to maintain the equipment they already have. Half of respondents have adopted fleet management technology, up from 34% last year, and they report much greater comfort with related tools and concepts.

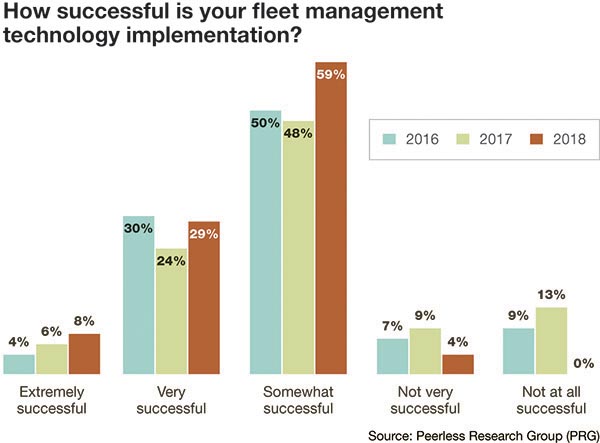

After 22% of those surveyed last year said their fleet management technology implementation was “not very” (9%) or “not at all” successful (13%), now 4% report “not very” and none have deemed it a complete failure.

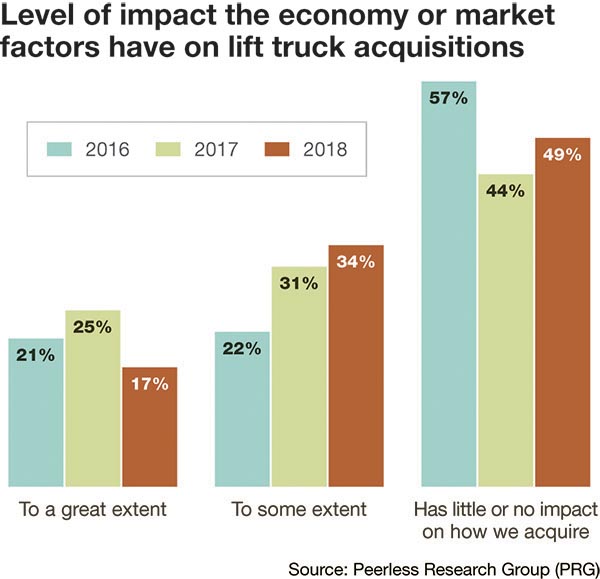

Optimism is on display elsewhere in the survey, particularly with regard to economic and market factors. When asked to what extent these factors influence buying decisions, a quarter of last year’s responded said “to a great extent.”

Optimism is on display elsewhere in the survey, particularly with regard to economic and market factors. When asked to what extent these factors influence buying decisions, a quarter of last year’s responded said “to a great extent.”

Now, just 17% heavily weigh the economy before acquiring equipment, and 49% claim it has little or no impact on their decision-making. Short answer sections captured examples of the reasoning behind each response.

Great impact:

- Higher sales volume gives more justification for forklift investment.

- We are allowed a budget, and that usually is the first thing to get slashed.

- When the economy is doing well, we do well and need to upgrade some of our older units.

Some impact:

- We regularly replace lift trucks. The economy will affect how many of each class we will replace.

- Depends on cost and whether we can maintain revenues.

- We’ll delay new leases if the economy is down.

No impact:

- If they are due to be replaced, we replace them.

- It depends on our requirements and must align with the plant’s goals and strategy.

- When the machines start costing too much to fix, they’re replaced.

Different strokes

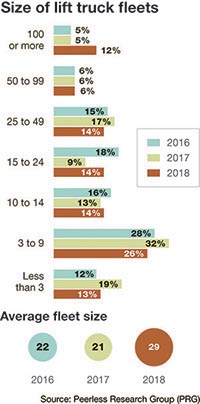

This year’s group of respondents includes significantly higher representation from large fleets of more than 100 units (12%, up from 5%), and less from small fleets of fewer than 10 (39%, down from 51%). Respondent demographics result in clear impacts to several survey results, such as preferred sales channels. Whereas last year’s survey indicated 87% work with dealers and 14% purchase direct from the manufacturer, those figures have shifted to 82% and 23%, respectively.

Similarly, a survey base of large fleets has dramatically impacted the ratio of units bought versus leased. Last year, 60% of respondents indicate they buy equipment, 9% lease and 31% do a bit of both. All told, 79% of lift trucks were bought outright and 21% leased. This year, with just 15% of respondents both buying and leasing, the total number of units acquired each way is closer

to 50/50.

Reasons for buying:

- Strictly a financial/accounting decision (43%).

- Cheaper (37%).

- Low-usage equipment (32%).

Reasons for leasing;

Reasons for buying and leasing;

The demographics of this year’s survey base might also be reflected in the percentages of new lift trucks that will expand fleet size as opposed to replace existing units. Last year, 58% of acquisitions were replacements as 42% would grow the fleet. This year replacements will account for 68% of purchases, while just 32% represent additions to fleet size.

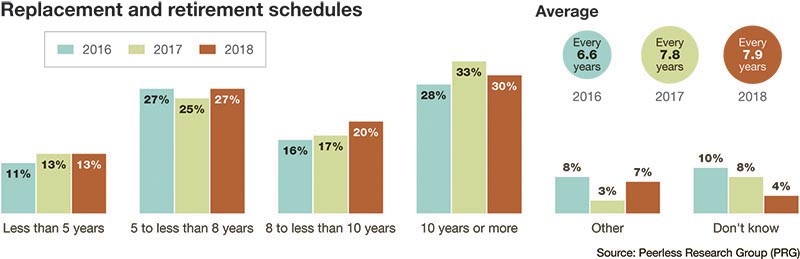

Despite results suggesting strong replacement activity, the average replacement cycle was again close to eight years, with roughly the same number of respondents indicating they typically replace forklifts within five years (13%), between five and eight years (27%), eight and 10 years (20%) or more than 10 years (30%). And, 4% said they don’t know, down from 10% just two years ago.

When it comes time to dispose of equipment, owners resell nearly half of outgoing units. A third are returned to the dealer when it drops off new equipment, and a quarter are stored “just in case.” About 18% are kept for parts.

What’s in a fleet

Electric-powered rider trucks are now present in almost 70% of fleets, a record high that illustrates the growing popularity and capability of electric equipment. These Class 1 trucks include counterbalanced, sit-down and stand-up types.

The next largest category is Class 3 electric-powered walkies, riders, low- and high-lift and reach types, which are present in more than 60% of all fleets.

Class 2 electric narrow-aisle trucks, orderpickers, turret trucks and stackers are in 44% of fleets, followed by internal combustion, counterbalanced, cushion-tire lift trucks in 36% of fleets.

Beginning last year, the survey also asks about the adoption of autonomous or semi-autonomous forklift technology. For example, “dual mode” equipment can be operated manually but might also have an autonomous mode for non-value-added travel. Another example is a remote control that allows a picker to advance a pallet jack without touching it.

Beginning last year, the survey also asks about the adoption of autonomous or semi-autonomous forklift technology. For example, “dual mode” equipment can be operated manually but might also have an autonomous mode for non-value-added travel. Another example is a remote control that allows a picker to advance a pallet jack without touching it.

Last year, 11% reported they are either using or evaluating such technologies, a number that has climbed to 14%. The practice of dividing equipment into a core, regularly used fleet and a less-utilized reserve fleet is gaining traction. Half of respondents report operating a core fleet, up from 40% last year.

To keep the wheels in motion, 75% of respondents expect to purchase wheels and tires in the coming year, as well as batteries and battery accessories (65%), brake components (49%), safety equipment (36%), chains (20%) and forks (20%).

Training and service

Once again, four out of five respondents use an internal training program to keep forklift operators up to speed. The percentage of those who turn to dealers (15%) or independent trainers (14%) each shed roughly 5% since last year.

Meanwhile, the appetite for in-house maintenance programs continues to decline.

Just one in five say internal staff handle lift truck maintenance, down from the one in three reported four years ago. About half still outsource service to a lift truck dealer, and 23% outsource to a maintenance or service contractor.

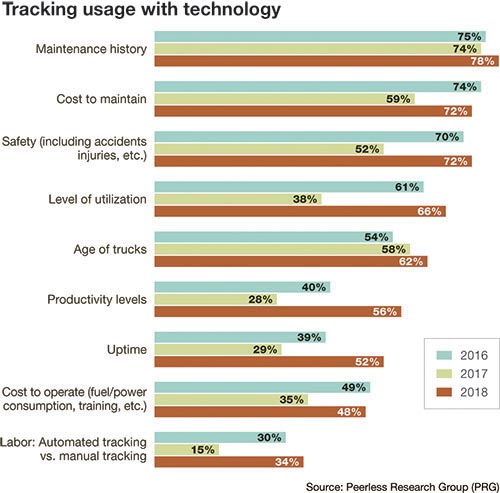

Among the 50% of respondents using fleet management technologies, key priorities include maintenance history (78%), cost to maintain (72%), safety (72%), productivity (56%) and automated labor management (34%). Although adoption and satisfaction with fleet management technologies continue to grow, fleet managers are still in the relatively early phases of transitioning from reactive to proactive maintenance.

In a short answer section, respondents offered the following insights.

Biggest challenges in implementing or using a fleet management software solution:

- Actually using the data.

- Employee education, operator buy-in, maintenance staff training.

- Knowing damage versus wear and tear.

- Labor, productivity and safety portions not yet implemented.

- Lack of standardization between manufacturers.

- No resources to monitor the system and produce reports to process owners.

Reasons for not using or pursuing fleet management technology:

- We handle this internally.

- I have used it in the past, and it is more trouble than it is worth. It takes too much time to manage the system.

- Cost, ROI.

- I’m not aware of this technology.

- We are not familiar with the software. We currently use homemade spreadsheets.

Survey methodology and demographics

This year’s survey was sent to lift truck users across the industry by Peerless Research Group (PRG). Of the 114 qualified respondents with active fleets, 38% are located in a manufacturing plant while others either work in a warehouse facility (16%) or distribution center (37%).

A qualified response is someone personally involved in the evaluation, selection and procurement of lift trucks at their facility. With 70% of respondents in the manufacturing industry, a range of industry sectors are represented, including food and beverage, plastics and rubber, automotive and transportation equipment, textiles, electronics, etc.

One out of six work in wholesale or retail trade. The respondents represent a cross-section of company size, averaging 29 lift trucks in operation, 368 employees and $878 million in revenues.