The iPhone’s 8th Anniversary

Smartphones existed before Steve Jobs introduced the iPhone on January 9th, 2007. But by upending existing technology platforms he kick-started a new era of computing whose impact is yet to be fully understood.

Eight years ago, Steve Jobs walked onto the stage at MacWorld San Francisco and gave a masterful performance (view video above).

His presentation is worth revisiting from time to time, a benchmark against which to evaluate a PowerPoint-addled CEO pitch or a product intro cum dance number.

In his talk, Jobs tells us that the iPhone is one of these products that, like the Mac and the iPod before, “changes everything”. He was right, of course, but one wonders… even with his enormous ambition, did Jobs envision that the iPhone would not only transform Apple and an entire industry, but that it would affect the world well beyond the boundaries of the tech ecosystem?

If the last sentence sounds a bit grand, let’s look at the transformation of the smartphone industry, starting with Apple.

In 2006, the year before the iPhone, Apple revenue was $19B (for the Fiscal Year ending in September). That year, iPod revenue exceeded the Mac, $7.7B to $7.3B…but no one claimed that Apple had become an iPod company.

In 2007, revenue climbed to $24B, a nice 26% progression. Mac sales retook the lead ($10.3B vs. $8.3B for the iPod), and iPhone sales didn’t register ($123M) as shipments started late in the Fiscal Year and accounting’s treatment of revenue blurred the picture.

In 2008, revenue increased to $32.5B, up 35%. iPhone revenue began to weigh in at $1.8B, far behind $9B for the iPod and $14.3B for the Mac (a nice 39% uptick).

In 2009, revenue rose by a more modest 12%, to $36.5B - this was the financial crisis. iPod declined to $8B (- 11%) as its functionality was increasingly absorbed by the iPhone, and the Mac declined a bit to $13.8B (- 3%). But these shortfalls were more than compensated for by iPhone revenue of $6.8B (+ 266%), allowing the company to post a $4B increase for the year. This was just the beginning. (And even the beginning was bigger than originally thought: Due to a change in revenue recognition esoterica, 2009 iPhone revenue would be recalculated at $13.3B.)

In 2010, iPhone revenue shot up to $25B, pushing Apple’s overall revenue up by a phenomenal 52% to $65B. The iPhone now represented more than 1/3rd of total revenue.

In 2011, growth accelerates, revenue reaches $108B (+ 66%), more than five times the pre-iPhone 2006 number. iPhone reaches $47B (+ 87%), now almost half of the company’s total.

For 2012, sales shoot up to $156.5B (+ 45%), and the iPhone reaches $80.5B (+ 71%). At such massive absolute numbers, 45% and 71% growth look almost unnatural as they appear to violate the Law of Large Numbers. As this happens, the iPhone crosses the 50% of total revenue threshold, and accounts for probably 2/3rd of Apple’s total profit.

Apple’s growth slowed in 2013 to a modest + 9%, with $171B overall revenue. The iPhone, weighing in at $91.3B (+ 16%), provides most ($12.6B) of the modest ($14B) overall revenue increase and 53% of total sales.

Last year, growth slows just a bit more: $182.8B (+ 7%) with the iPhone reaching $102B (+12%). Once again, the iPhone contributes most of the total revenue growth ($10.7B of $11.9B) and fetches 56% of the company’s sales. Notably, the iPad shows a 5% decrease and, at $2.3B, the iPod is becoming less and less relevant. (Although, how many companies would kill for $2.3B in music player revenue?)

The excellent Statista portal gives us picture of the iPhone’s emergence as Apple’s key product:

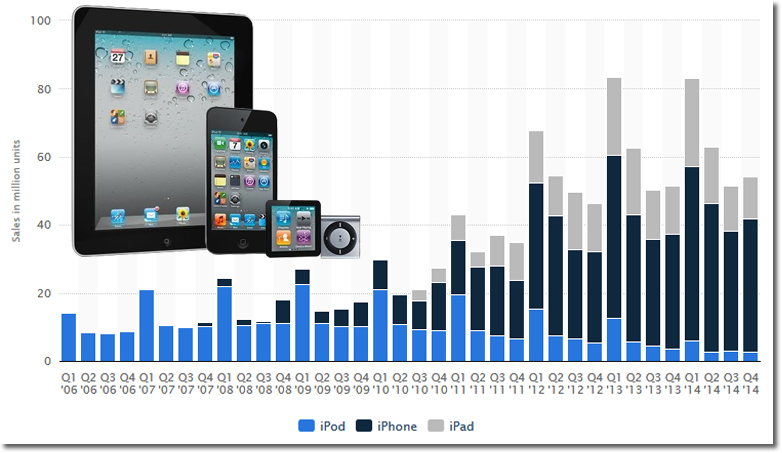

iPhone, iPad and iPod sales from 1st quarter 2006 to 4th quarter 2014 (in million units)

Here you can see a comparison of Apple iPhone, iPad and iPod sales from the first quarter of 2006 to the company’s latest financial quarter. It has been suggested that the development of the iPhone has led to the cannibalization of the iPod, and that Apple is effectively making one of their own products obsolete. As can be seen in the graph, quarterly iPod sales have slightly decreased as iPhone and iPad sales have increased.

While the company is about ten times larger than it was before the iPhone came out, the smartphone industry has become a nearly trillion dollar business. Depending on how we count units and dollars, if we peg Apple at 12% market share, that means the worldwide number across the smartphone industry reaches $800B. If we grant Apple just a 10% share, we have our $1T number.

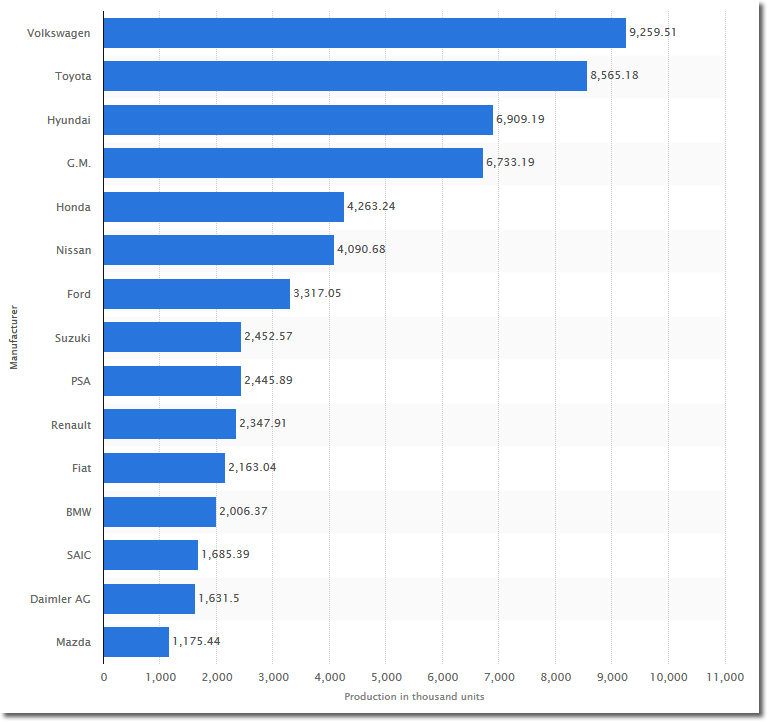

For reference, still according to Statista, the two largest auto companies, Toyota and the Volkswagen Group, accounted for $485B in revenue in 2013:

Leading passenger car manufacturers worldwide in 2013, based on production (in 1,000 units)

The statistic shows the world’s leading passenger car manufacturers in 2013, based on production. Volkswagen produced about 9.3 million vehicles in 2013. China’s SAIC produced some 1.7 million passenger cars in 2013.

However we calculate its size, whether we place it at $800B or $1T, what we mustn’t do is think that the smartphone industry merely grew to this number. Today’s smartphone business has little in common with what it was in 2006.

Consider that Motorola “invented” the cell phone. Now Motorola is (essentially) gone: Acquired by Google, pawned of to Lenovo, likely to do well in its new owner’s Chinese line.

Nokia: The Finnish company stole the crown from Motorola when cell phones became digital and once shipped more than 100M phones per quarter. Since then, Nokia was Osborned by its new CEO, Stephen Elop, an ex-Microsoft exec, and is now owned by Elop’s former employer. With 5% or less market share, Nokia is waste of Microsoft resources and credibility… unless they switch to making Android phones as a vehicle for the company’s “Cloud-First, Mobile-First” apps.

Palm, a company that made a credible smartphone by building on their PDA expertise, was sold to HP and destroyed by it. They’re worse than dead, with a necrophiliac owner (TCL), and LG humping other parts of the corpse for their WebOS TVs and a WebOS smartwatch.

And then there’s the BlackBerry. Once the most capable of all the smartphones with a Personal Information Manager that was ahead of its time, it was rightly nicknamed CrackBerry by its devoted users. Now BlackBerry Limited is worth less than a 1/100th of Apple, and is trying to find a niche – or a seeker of body parts.

Related: 3 Leadership Lessons from Amazon’s (Jeff Bezos’s) Fire Phone Fiasco

The change in the industry is, of course, far from being solely Apple’s “fault”. In many ways, Google destroyed more incumbents than Apple. Google acquired Android in 2005, well before the iPhone appeared. According to the always assertive Tomi Ahonen, China now sports more than 2000 (!) phone brands, all based on some Android derivative. And let’s not forget the voraciousness of Apple’s giant Korean frenemy Samsung, which acts as both a supplier of key iPhone components and a competitor.

But is the industry now settled? Are any of the current incumbents, including Apple, unassailable? Market-leading Samsung appears to be challenged by both Apple at the high end and Xiaomi from below, and has announced more recent troubles. Our friend Tomi argues that Xiaomi isn’t the new Apple but that Lenovo and Huawei are the ones to watch. And, of course, Apple is seen as a “hits” company, a business that lives and dies by its next box-office numbers - and the numbers for the new iPhone 6 aren’t in, yet They’re likely be very strong.

Regardless of any individual company’s business case, the overall of impact of the smartphone on the world is what counts the most. In a blog post titled Tech’s Most Disruptive Impact Over the Next Five Years, Tim Bajarin argues that the real Next Big Thing isn’t the Internet of Things, Virtual Reality, or BitCoin. These are all important advances, but nothing compared to the impact of smartphones [emphasis mine]:

“Another way to think of this is that smart phones or pocket computers connecting the next two billion people to the internet is similar to what the Gutenberg Press and the Bible were to the masses in the Middle Ages.”

As Horace Dediu notes, we’re on track to 75% US smartphone penetration by the end of 2014. The big impact to come will be getting the entire world to reach and exceed this degree of connectivity, especially in areas where there’s little or no wired connectivity.

This is what Steve Jobs started eight years ago by upending established players and carrier relationships.

Source: Monday Note

Related: 3 Leadership Lessons from Amazon’s (Jeff Bezos’s) Fire Phone Fiasco

The World is Going Mobile

As I look at where the technology industry is going, it is clear it is increasingly mobile. What is after mobile? More mobile. What the shape and form of those mobile devices will be is another question but they will still be mobile devices. How we interact with software, services, the internet, each other, may all look different than today but it will still be within a mobile paradigm. Mobile is becoming the foundation for everything - hardware, software, and services.

Download the White Paper: The Next Phase in Mobile

Article Topics

Creative Strategies News & Resources

The Next Phase of Mobile The iPhone’s 8th AnniversaryLatest in Technology

SAP Unveils New AI-Driven Supply Chain Innovations U.S. Manufacturing is Growing but Employment Not Keeping Pace The Two Most Important Factors in Last-Mile Delivery Spotlight Startup: Cart.com is Reimagining Logistics Walmart and Swisslog Expand Partnership with New Texas Facility Taking Stock of Today’s Robotics Market and What the Future Holds Biden Gives Samsung $6.4 Billion For Texas Semiconductor Plants More Technology