Supply Chain Transparency a Challenge: KPMG Outlook Report

KPMG's 2014 Global Manufacturing Outlook Report forecasts an 'Era of Disruptive Complexity' focused on profitable growth through innovation, collaboration and supply chain integration.

Manufacturers are entering into a new era of ‘disruptive complexity’ which is fundamentally changing the way they compete and succeed, according to the KPMG’s 2014 Global Manufacturing Outlook (GMO).

“Over the past few years, manufacturers have seen an explosion of new technologies and innovative developments in material science, advanced manufacturing and synergistic operating models.

With this accelerating pace of change, manufacturers the world over are now starting to take stock of the more complex world that they are operating in, and are using that insight to redefine ‘the art of the possible’,” noted Jeff Dobbs, Global Chair, Industrial Manufacturing and a Partner with KPMG in the US.

In an attempt to capitalize on this environment, manufacturers say they will dramatically increase spending in R&D, pursue new collaborative business models and integrate new technologies to analyze and stimulate profitable growth.

This fifth annual Global Manufacturing Outlook, Performance in the Crosshairs, was completed in early 2014 and surveyed 460 senior executives across six industrial sectors split equally among the Americas; Europe, Middle East and Africa; and Asia-Pacific.

Related: 5 Factors for Achieving Manufacturing Excellence in Good Times or Bad

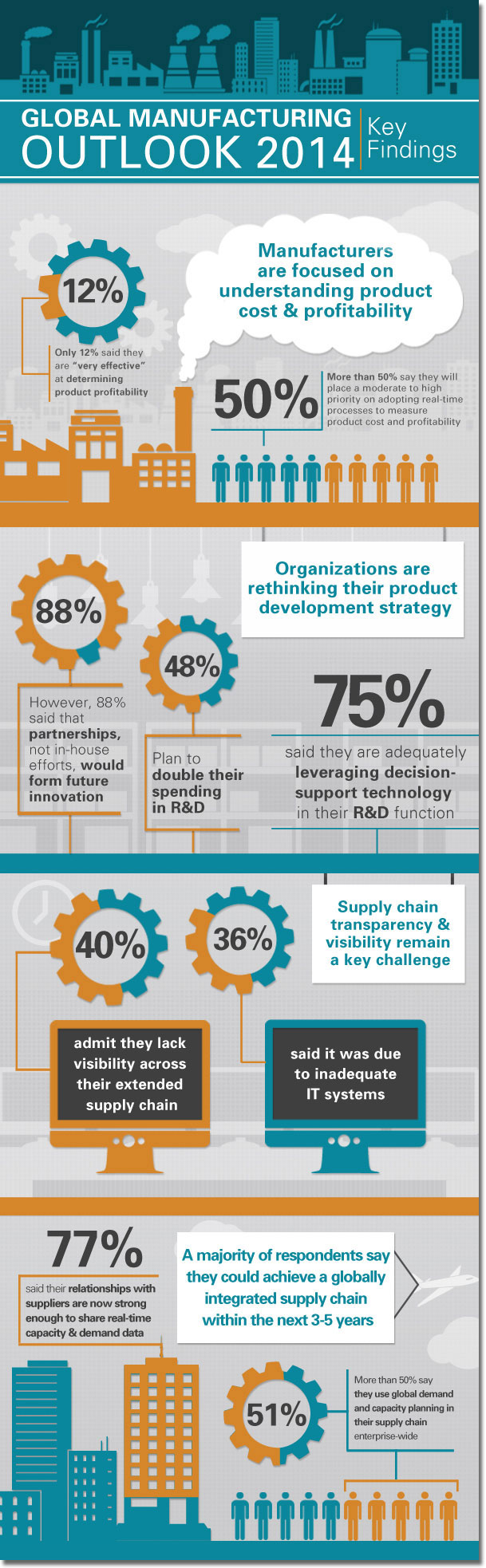

A focus on understanding profitability

This year’s GMO reveals that only 12 percent of manufacturers would categorize themselves as being ‘very effective’ at determining product profitability. Further, 85 percent of respondents said they plan to make either “moderate” to “substantial” investments into systems for product or service cost improvement over the next 12-24 months.

“This isn’t simply about mining data and building spreadsheets; it’s about accessing the appropriate information, at the right level of granularity and – maybe most importantly – with the right speed and frequency to generate timely insights that help people make better business decisions,” noted Jim Scalise, a Management Consulting Partner with KPMG in the US.

Growth through innovation and collaboration

According to the KPMG’s 2014 GMO, almost half of manufacturers plan to double R&D spending in product development over the next 12-24 months. There are also signs that breakthrough innovation is gaining importance as a strategy for 39 percent of industrial manufacturers, up 8 percentage points from KPMG’s 2013 GMO, representing a 25 percent increase in companies pursuing such strategies.

“The manufacturing world is in an era of hyper-innovation,” said Dobbs. “Ultimately, those organizations that do not balance investment in ‘incremental innovation’ with investment in ‘breakthrough innovation’ may find themselves left behind competitively.”

Manufacturers in Germany appear set to lead in breakthrough innovation with 77 percent citing it as their primary R&D strategy for product development. Among the industrial sectors included in the survey, 50 percent of respondents from the Conglomerates sector say breakthrough innovation will be their primary R&D strategy.

In terms of business models, 88 percent of respondents say partnerships over in-house efforts will shape manufacturers’ approach to innovation, up significantly from 51 percent in KPMG’s 2013 GMO. Additionally, 68 percent say they are adopting more collaborative business models with suppliers and customers. In EMEA, respondents were overwhelmingly in strong agreement with adopting more collaborative models (82 percent).

Improving supply chain visibility

This year’s GMO reveals that limited visibility across the supply chain remains a growing concern for manufacturers, even though many have made notable progress towards improving transparency.

Forty percent – versus 20 percent in KPMG’s 2013 GMO – say they lack information and material visibility across their supply base. Thirty eight percent say they lack critical details on supplier performance, and 36 percent lack adequate supply chain IT systems. According to half of respondents, the biggest obstacle to achieving more visibility is a lack of mature technology, followed by lack of governance (19 percent) and lack of strategy (14 percent).

Despite those challenges, visibility has improved over the past twelve months with 22 percent of respondents now claiming to have complete visibility (up from just 9 percent in 2013). For the most part, these gains in visibility have resulted from stronger relationships between manufacturers and their top tier suppliers. More than three quarters of respondents say that their relationship with top tier suppliers is now strong enough for them to share real-time capacity and demand data.

“The upward trend is promising given the fact that almost three quarters of our respondents think they can achieve a globally integrated supply chain within the next five years,” Dobbs said. “However, we believe there is still much work to be done around trusted relationships, transparency, and technology enablement to foster these types of collaborative business models“.

Download the Report: Global Manufacturing Outlook 2014: Performance in the Crosshairs

Article Topics

KPMG News & Resources

Supply Chain Stability Index sees ‘Tremendous Improvement’ in 2023 Supply Chain Stability Index: “Tremendous Improvement” in 2023 Supply chain stability remains elusive, notes new report from ASCM and KPMG Elevated freight and labor costs remain issues for stressed out supply chains New index by ASCM and KPMG shows supply chain stress level more than doubled in past two years DoD picks KPMG to assist on 5G application for Marine Corp’s smart warehouse project Conventional warehouse tune up More KPMGLatest in Supply Chain

How Supply Chains Are Solving Severe Workplace Shortages SAP Unveils New AI-Driven Supply Chain Innovations How Much Extra Will Consumers Pay for Sustainable Packaging? FedEx Announces Plans to Shut Down Four Facilities U.S. Manufacturing is Growing but Employment Not Keeping Pace The Two Most Important Factors in Last-Mile Delivery Most Companies Unprepared For Supply Chain Emergency More Supply Chain