Size of Company Does Not Make an Organization a Master of Logistics

Karl B. Mandrodt, Ph.D., Mary Collins Holcomb, Ph.D., and Rob Estes, President & CEO, Estes Express Lines, apply the findings of the 23rd Annual Trends & Issues in Transportation and Logistics Study to the world of transportation and logistics shipper-carrier decision making.

Results from the annual survey suggest that carriers, driven by a need to maximize profitability, are at a polar opposite with shippers who are focused on reducing costs (Video Above).

This lack of alignment has created a struggle that has resulted in a loss of focus on the bigger prize - being able to compete supply chain to supply chain.

The analogies between the game of “tug of war” and the current state of freight transportation management are almost boundless. Increasing transportation costs driven by a host of factors has now created a struggle between shippers and carriers as each side seeks to achieve their goals.

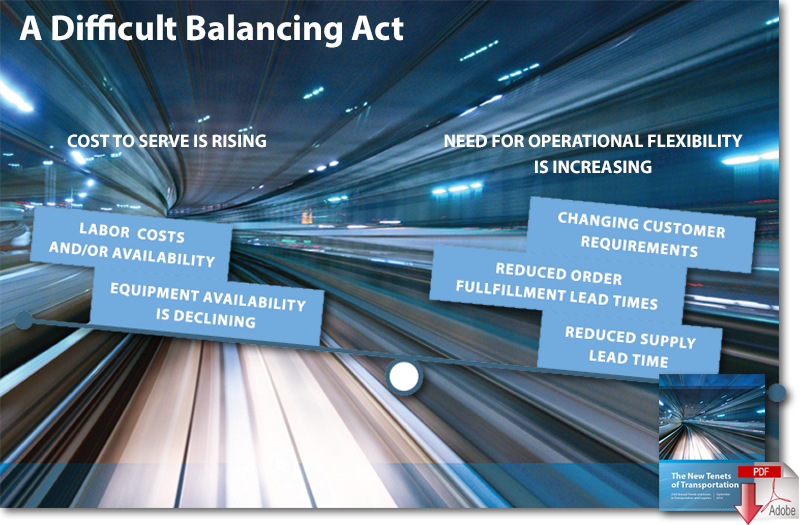

In fact, the results of the 23rd Annual Study of Trends and Issues in Transportation and Logistics neatly define the tussle, where carriers are pulling hard to maximize their profitability while shippers are focused on reducing rising transportation costs.

Shippers are being pulled into higher rate territory as carriers deal with the impact of compliance, a driver shortage, and increased demand - all of which are driving up their costs.

And to make the situation worse, constantly changing customer requests coupled with increasing demand uncertainty has created an environment where the only constant is uncertainty.

Results from this year’s annual study further point out why the tug of war between shippers and carriers is not a winning game plan for either party.

To address these challenging conditions, shippers are working on increasing their operational flexibility. The data show that companies have identified several key initiatives as being the most important in assisting them to achieve greater flexibility.

These are: reducing order fulfillment lead times and supply lead times, integrating internal processes, and increasing collaboration with key customers and suppliers.

How do these priorities line up with completed initiatives? In many ways, they are quite different.

The results show deployment of multiple modes of transportation is the most frequently completed action by companies to increase their agility and responsiveness. To date, 45.9 percent of companies have finished implementing this initiative.

Most Frequently Completed Flexibility Initiatives

- Utilization of multiple transportation modes

- Alignment of labor force skills to better meet changing demand requirements

- Shared capacity forecasts and increased collaboration with key customers

Many of the more difficult initiatives - and some of the most important ones - to improve operational flexibility are underway, including the integration of internal processes and increased collaboration with key suppliers.

It’s clear that both parties agree that price is a major factor when choosing a strategic/core carrier. Further, they agree that many of the transportation services provided are highly standardized, which in turn makes standardization of the processes and procedures more straightforward. These factors point to a commoditization of transportation.

While at first glance commoditization of transportation services may seem like a viable avenue for shippers to reduce costs, it may be more costly in the long run as continuous improvement and differentiation of service are needed to compete. For carriers, commoditization will likely drive the relationship to a more transactional one with an emphasis on price.

However, the study results also reveal where opportunity gaps exist to stop the progression towards commoditization.

Article Topics

University of Tennessee Center for Executive Education News & Resources

Why Universities Need to be More Agile University of Tennessee, Knoxville Launches Online Master’s in Supply Chain Management McDonald’s “Secret Sauce” for Supply Chain Success Selecting and Managing a Third Party Logistics Provider Unpacking Risk Shifting Shortfalls in the Management of Third-Party Logistics The ABCs of DCs Distribution Center Management More University of Tennessee Center for Executive EducationLatest in Transportation

FedEx Announces Plans to Shut Down Four Facilities The Two Most Important Factors in Last-Mile Delivery Most Companies Unprepared For Supply Chain Emergency Baltimore Bridge Collapse: Impact on Freight Navigating Amazon Logistics’ Growth Shakes Up Shipping Industry in 2023 Nissan Channels Tesla With Its Latest Manufacturing Process Why are Diesel Prices Climbing Back Over $4 a Gallon? More Transportation