Rising Peak Season volumes and rates are intact, says Flexport

As it indicated in its previous report, data recently issued by San Francisco-based freight forwarding and customs brokerage services provider Flexport in its July 2017 Market Update continues to pinpoint the pairing of rising volumes and rates with Peak Season here.

As it indicated in its previous report, data recently issued by San Francisco-based freight forwarding and customs brokerage services provider Flexport in its July 2017 Market Update continues to pinpoint the pairing of rising volumes and rates with Peak Season here.

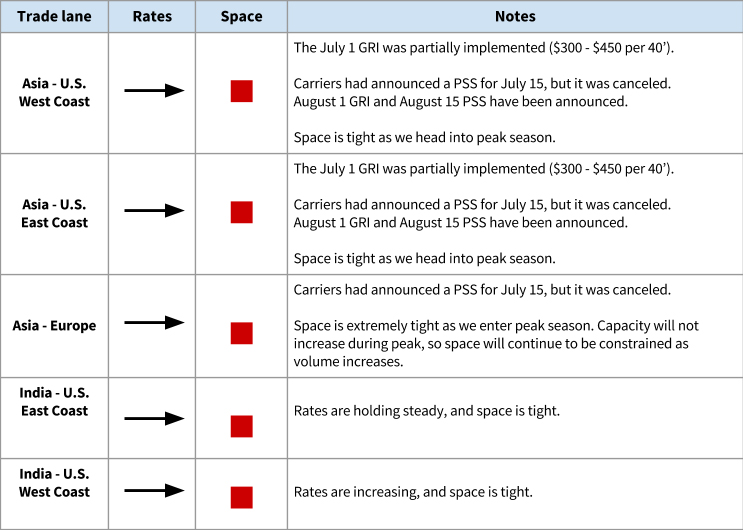

In its report, Flexport presented an outline of ocean rates and related capacity availability for various lanes, including:

- Asia -U.S. West Coast, with “space extremely tight as we head into peak season” and the August 1 GRI introduced at $650 per FEU (Forty foot equivalent unit), which will be implemented at $500-$600 per FEU, and carriers announcing Peak Season Surcharges (PSS) for August 15 at $540, $600, $675, and $765 for 20’, 40’, 40’ HC (High Cube), and 45’, which Flexport is monitoring to see if rates will be mitigated;

- Asia-U.S. East Coast, with extremely tight heading into peak season, and an August 1 GRI announced at $650 per FEU, which will be implemented at $500-$600 per FEU, and carrier PSS for August 15 at $540, $600, $675, and $765 for 20’, 40’, 40’ HC (High Cube), and 45’, which which Flexport is monitoring to see if rates will be mitigated;

- Asia-Europe, with space extremely tight entering peak season, and carriers’ PSS fort August 1 at $200, $400, $400 for 20’, 40’ and 40’ HC that some carriers have implemented at a mitigated rate and some not implementing it, and Flexport said that carriers with less BCO volume support will keep rates more flat and those with more BCO volume will move rates slightly up;-India-U.S. East Coast, with rates increasing and space tight heading into peak season, with Flexport monitoring a GRI that was implemented on August 7; and

- India-U.S. West Coast, with rates increasing and space very tight heading into peak season

Aside from peak season pricing, the few large ocean carrier alliances also have a direct influence on both pricing and capacity, and Flexport COO Sanne Manders explained that at this point, all three ocean carriers alliances (2M, Ocean Alliance, The Alliance) are full and rolling cargo the United States West Coast and less full to United States East Coast.

“This is peak season, when the carriers are full,” he said. “Carriers manage space independently within the alliances. Every carrier has a different strategy, some carriers have 70-80% fixed business and have very little room to accommodate additional freight. Others fully rely on spot cargo and they might have more space available during peak. Most of the carriers work on allocation basis where you get space based on historical support & commitment. What Flexport does differently is being very reliable to carriers. Typically forwarders overbook (double bookings on multiple carriers) and cancel up to 50%. We have much better forecasting and therefore cancel way less, less than 5%. Carriers reward reliability by providing allocations / space protection. Price and allocation are two sides of the same coin, but most forwarders only book on price. We book on a pricepoint at an available inventory. Some carriers also overbook a lot more than others, similar to airlines.”

Last month, Manders told LM that there was some anxiety in the in the market with the new contract prices expected to be higher, with retailers and bigger shippers pre-loading in advance of peak season” followed by prices dropping around June 1and GRI/PSS then heading up a bit for peak.

And now with July 1 and August 1 GRIs implemented, he said rates are 30%-to-40% higher today than they were in June, with more increases also expected between mid-August through the end of September into mid-October.

On the air cargo side, Flexport noted that 2017 has been a “huge” year for airfreight, with rates staying high and expected to head up further during peak season, as demand has continued to outpace supply.

And it added that the Trans-Pacific air market is especially strong, citing how United Cargo’s revenues rose 22%, due to increased volumes.

“Demand outpacing supply means that spot prices go up very quickly and capacity is tight, which means delays,” explained Manders. “Interestingly enough, not all days are as busy in air cargo. Typically Thu/Fri/ Sat/Sun are more wanted than Mon/Tue/Wed. This has to do with production runs of the factories. When end of week flights are totally full, roll overs to flights in early next week become very common.”