Automation Study: The State of Automation

As automation makes its way into more warehouses and DCs, a growing number of companies told Modern they’re looking to upgrade existing or add new equipment and software over the next two years.

The image of the autonomous warehouse is coming into clearer focus as more hardware and software manufacturers develop innovations that remove much of the “human” component from the distribution process. From flexible shuttle systems to robotics equipped with embedded intelligence to automatic guided vehicles (AGVs), warehouses and DCs around the globe are becoming a hotbed for automation implementation and experimentation.

And while the number of innovations and pioneering approaches implemented by e-tailing giant Amazon are becoming humdrum, one can hardly argue with the company’s early adoption of automation for warehouse picking and packing. Having acquired Kiva Systems in 2012, the e-tailer is automating its fulfillment center operations with features like autonomous mobile robots, control software, language perception, machine learning, object recognition, and semantic understanding of commands, according to Amazon Robotics’ Website.

The question is, what is the rest of the manufacturing, distribution and logistics community doing on the automation front? And, how are companies putting these solutions to good use in today’s fast-paced distribution environment? To find out, Peerless Research Group (PRG), on behalf of Modern Materials Handling, conducted a survey to assess the usage and purchase intentions for automation systems and solutions used in warehouse and DC operations.

For the report, Modern looked at factors and features considered important when evaluating automation systems and solutions for possible purchase; the extent to which specific warehouse processes are automated; areas that operations will be looking to improve during the next two years; order fulfillment activities currently running; and tasks companies will look to improve/implement. Here’s what we learned.

The case for automation

With primary operations in industries like food, beverage, tobacco, automotive/transportation, chemicals/pharmaceuticals, industrial machinery, and paper/printing, respondents to the survey had warehouse/DC operations spanning 50,000 square feet or less (29%) all the way up to 250,000 square feet or more (29%). Most of the facilities (44%) employ fewer than 100 people, and 32% have 100 to 499 workers, with the average across all respondents being 658 workers. The bulk of respondents (30%) work for firms where revenues are less than $10 million, while 18% have $10 million to $49.9 million, and 13% have between $1 billion and $4.9 billion in average revenues. The average annual revenue for respondents was $872 million.

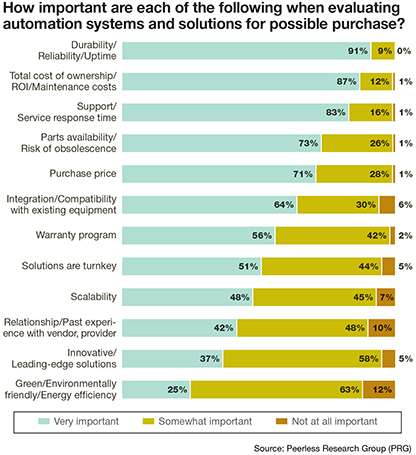

Of the 221 respondents who took part in the automation survey in January and February of 2017, most (91%) see durability, reliability and uptime as the most important criteria when evaluating automation systems and solutions for possible purchase. Other key yardsticks that come into play include total cost of ownership (TCO), return on investment (ROI), and maintenance costs (87%); support and service response time (83%); and parts availability and risk of obsolescence (73%). Factors like purchase price, integration with existing equipment and warranty were further down the list.

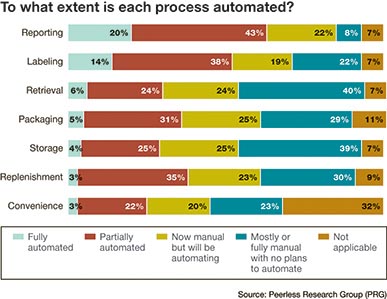

Asked to what extent numerous processes are currently automated, respondents said their fully automated systems include reporting (20% of participants), labeling (14%), retrieval (6%) and packaging (5%). And, 43% of companies have partially automated reporting systems, while 38% have partially automated their labeling systems. The top warehouse and DC systems that companies plan to automate in the near future include packaging (25%), storage (25%), retrieval (24%) and replenishment (23%).

Over the next two years, respondents want to improve their warehouse capacity utilization (65%), picking efficiency or lines picked per hour (63%), labor reduction (60%), order accuracy (60%) and order cycle time (50%).

Addressing a fast-paced business world

In the fast-paced e-commerce and omni-channel distribution environment, companies are handling numerous different fulfillment activities in their warehouses and DCs. Eighty-six percent use their facilities for warehousing and storage; 64% for individual pick, pack and ship wholesale distribution fulfillment; 59% for full and mixed pallet load fulfillment; and 57% for case and mixed case fulfillment.

When asked which operations they plan to improve over the next two years, 37% of respondents said they want to do a better job with individual pick, pack and ship for e-commerce fulfillment, and 34% would like to improve their case and mixed use fulfillment. Other areas in need of improvement include order customization, repacking and value-added services (34%); individual pick, pack and ship wholesale distribution fulfillment (33%); and full and mixed pallet load fulfillment (30%).

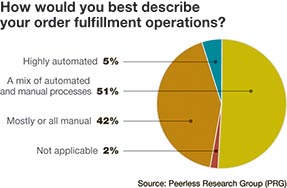

In describing their order fulfillment operations, the highest percentage of companies (51%) said they use a combination of automated and manual processes. Forty-two percent said they rely on mostly or all manual approaches, while 5% characterize their operations as being “highly automated.”

Conventional vs. automated, side by side

The modern-day warehouse and DC continues to rely heavily on conventional equipment and vehicles to run efficiently. For example, 93% of firms use lift trucks, 83% use storage and packaging equipment (e.g., palletizers, pallets/totes, bins, containers/rack, and shelving), and 82% use dock equipment. Fifty-six percent of respondents have no plans to upgrade or implement new equipment in this area right now, although 23% would like to enhance their storage and packaging, and 21% want to improve their hoists, cranes and monorails over the next 24 months.

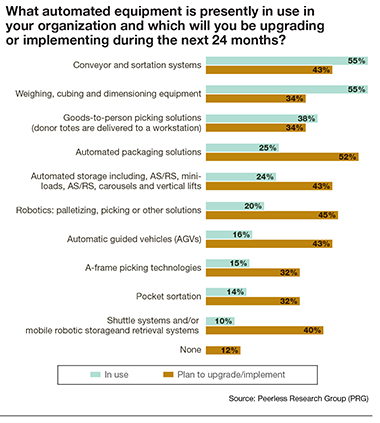

In terms of automated equipment, an equal number of respondents (55%) are using conveyor/sortation systems and weighing, cubing and dimensioning equipment. Thirty-eight percent use goods-to-person picking solutions (i.e., where donor totes are delivered to workstations); 25% use automated packaging solutions; and 24% rely on automated storage solutions like AS/RS, mini-loads, carousels and vertical lifts.

Over the next two years, 52% of companies want to either upgrade existing or implement new automated packaging systems, while 45% will focus on robotics (e.g., palletizing, picking or other solutions), and 43% are interested in conveyor and sortation systems, automated storage, and automatic guided vehicles. Other warehouse and DC automation that companies are interested in includes shuttle systems, goods-to-person picking solutions, and weighing/cubing/dimensioning equipment.

Right now, the automated equipment that is used most includes conveyor and sortation systems (55%); weighing, cubing and dimensioning equipment (55%); goods-to-person picking solutions (38%); and automated packaging solutions (25%). Over the next 24 months, the majority of respondents (52%) plan to upgrade or implement automated packaging solutions. Also of interest are robotics (45%), conveyor and sortation systems (43%), automated storage (43%), and automatic guided vehicles (43%).

The driving factors

Of those respondents that plan to evaluate or purchase automated materials handling equipment, technology or software over the next two years, the biggest driving factor is the need to fill orders faster to meet customer service level agreements and expectations. Other key reasons include the increase in piece picking and packing (driven by the growth in e-commerce orders); the need for new go-to-market strategies; and a drive to keep up with the competition (which is automating).

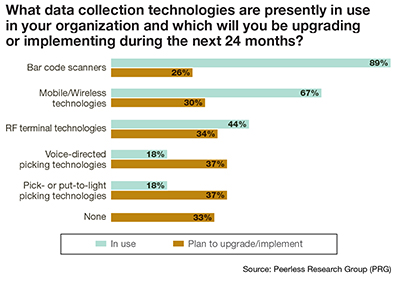

For data collection, the bulk of companies (89%) rely on bar code scanners while 67% are using mobile/wireless technologies. Forty-four percent use RF terminal technologies and 18% rely on voice-directed picking technologies. When asked which of these technologies they plan to integrate or upgrade over the next 24 months, an equal number of respondents (37%) are looking at voice-directed picking technologies and pick/put-to-light technologies. Another 34% of respondents want to use RF terminal technologies, 30% want to use mobile/wireless technologies, and 26% are interested in bar code scanners.

In terms of software, 78% of respondents use warehouse management systems (WMS), 39% use transportation management systems (TMS), 34% use warehouse control systems (WCS), and 31% rely on labor management systems (LMS). Of those companies that plan to upgrade or implement new supply chain execution software over the next 24 months, 34% plan to invest in WMS, 31% in parcel rating systems, and 30% in WCS.

When it comes to supply chain management software, 54% of companies use enterprise resource planning (ERP), 53% rely on order management systems (OMS), and 46% are using customer relationship management (CRM) solutions. Of the respondents that plan to upgrade or implement supply chain management solutions over the next two years, 29% will invest in supply chain planning (SCP), 29% in network design/optimization software, and 29% in CRM.

The dollars and cents

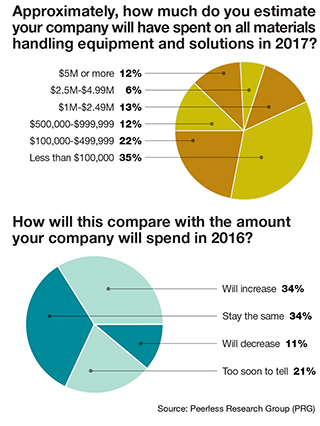

This year, most companies (35%) expect to spend less than $100,000 on all materials handling equipment and solutions, followed by 22% of companies that expect to spend $100,000 to $499,000. An equal number of respondents (12%) plan to allocate either $500,000 to $999,999 or $5 million or more to such investments. Thirty-four percent said this number is higher than 2016’s investment, while 34% said it would be the same as last year. Eleven percent of respondents said their 2017 investments would be lower than last year.

Asked about their existing sources of order fulfillment solutions, 64% said they work with distributors/dealers, 58% buy direct from the manufacturer, and 39% work with system integrators. For future purchases, the largest percentage of companies (60%) plan to work with system integrators while 52% and 51% (respectively) will work with distributor/dealers or manufacturers.

And, when handling the repair and maintenance of materials handling automated equipment, most companies (68%) rely on an internal maintenance crew. Forty-three percent use a service contract with their OEM and 39% use a service contract with a third party.